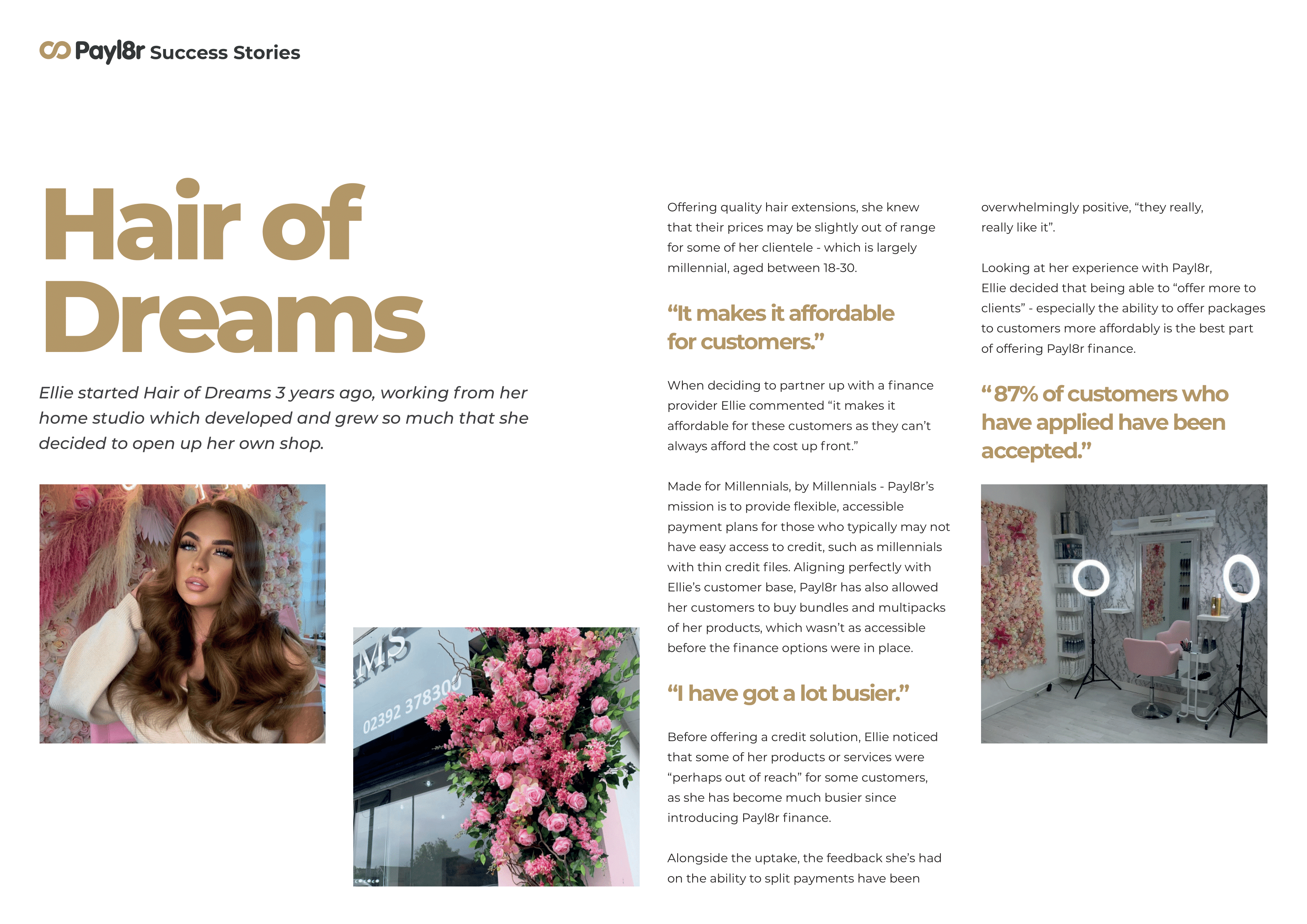

Open Banking: Why Does Payl8r Use It?

What is Open Banking?

A set of reforms and regulations, including the revised Payment Services Directive (PSD2) and the ruling issued by the UK Competition and Markets Authority (CMA) led to the fairly recent development of Open-Banking in the UK.

These changes allowed for a transformation of the way that financial data is shared and used between institutions to ultimately allow consumers access to a wider variety of products and services.

Authorised organisations can now access various transactional information such as your purchasing habits, any regular payments you make and the companies that you buy from. It’s important to note that this data can, and will only be shared with approved organisations after you have given permission. You will always be asked to provide authorisation before any data is shared.

Authorisation opens up a world of new financial apps and services to help consumers streamline their personal finances. Whether you’re self-employed and looking for an app to manage your money like Coconut, or you need an app that helps you stick to your monthly budgets such as Yolt, Open-Banking is the answer.

It’s clear that since the ‘launching’ of Open-Banking in the UK, there has been widespread interest in its opportunities as Openbanking.org states that there are now "over two million people and small businesses...using open banking-enabled applications across the UK" And as this technology continues to develop, we can only expect further transformations in the way we handle and access our financial data.

Why does Payl8r use Open Banking?

When Payl8r began in 2015, we set out to revolutionise the way finance was assessed. Committed to being responsible and ethical lenders, we wanted to offer those with thin credit files access to personal finance options, if they were able to afford repayments. This was particularly important for markets such as millennials, who may not have much credit history, but might have the means to pay monthly instalments.

Open-banking technology allows us to view an electronic copy of a bank statement with up to 90 days transactional data to assess an applicant’s affordability. By reviewing their monthly income, alongside their essential expenditure, we can determine whether they will be able to repay their loan.

Therefore, customers that traditionally would have been rejected for lack of a credit file, now have the option to submit their bank statements electronically to have their affordability evaluated. This process has allowed us to accept over 100,000 customers and continues to help fulfil our initial mission of revolutionising the personal finance industry.

Comments

Post a Comment